Evergreen funds are gaining popularity with both GPs and investors; for GPs they provide a permanent capital base, for investors they open access to private markets that were historically inaccessible. These vehicles allow investors to subscribe and redeem capital on a periodic basis, rather than committing to a fixed fund life. But as they go mainstream, the operational demands on fund finance teams are growing faster than most are prepared for. NAV accuracy, given this is the basis on which investors in an evergreen fund transact on an ongoing basis, is where the risk is most acute. Particularly for PE, there is one aspect that is often overlooked, but cannot be in an evergreen fund: the importance of getting the equity value of each portfolio investment right.

The growing popularity of evergreen funds

Evergreen funds are no longer a niche product. According to MSCI, these semi-liquid structures are rapidly approaching $500 billion in AUM, having grown more than 30% in the twelve months through September 2025 alone. Annual flows into evergreen funds have surged from just $10 billion in 2020 to a projected $74 billion in 2025, even as traditional closed-end fundraising has slowed. More evergreen funds launched in 2025 than in any previous year, and the pipeline of new products from large asset managers shows no sign of abating. In our conversations with clients, it is becoming clear that even mid-market managers are increasingly looking to tap into evergreens.

With that growth comes a set of operational demands that are significantly more onerous than in traditional closed-end funds.

The operational demands of evergreen funds

In a conventional closed-end fund, net asset value is fundamentally a reporting metric. It matters for ongoing performance reporting to LPs, but it does not always govern the economic outcome. In most cases, investors commit capital at the outset, and their returns are realised at exit of the portfolio held by the fund. The NAV reported in the interim is an estimate; the truth emerges when assets are sold.

Evergreen funds change this. Because investors can subscribe and redeem on a periodic basis throughout the life of the fund, the reported NAV becomes the basis on which investors transact. Every subscription and every redemption depends on it. An overstated NAV dilutes incoming investors. An understated NAV disadvantages those reedeming. As MSCI has noted in its research on private market evergreen structures, what was once merely a reporting metric now functions as a market-clearing price.

This creates two demands that did not previously exist with such urgency. First, NAV must be calculated frequently, typically monthly, and fund managers must have the operational capability to derive it at any point in time, including providing flash NAVs between formal reporting cycles. Second, the number must be accurate. It is not just a reporting metric that can be corrected next quarter or at year end; it has real financial implications attached to it.

Both demands are operationally challenging for private equity funds looking at evergreen structures.

Two halves of a private equity portfolio valuation

Private equity portfolio valuations broadly divide into two component parts. The first, enterprise valuation, is well understood. The second, equity valuation, is where many fund finance teams fall short, and where evergreen funds create risk for a GP.

Part 1: Deriving enterprise value

The first component, arriving at the enterprise value of each portfolio company, is well established in both practice and professional guidance. The IPEV Valuation Guidelines (updated December 2025, effective April 2026), the globally recognised standard for private equity fair value measurement, provide the governing framework. Under IPEV, valuation is grounded in fair value: the price that would be received in an orderly transaction between market participants at the measurement date.

In practice, this means three sequential workstreams: collecting portfolio KPIs and financial data ahead of each valuation cycle; sourcing relevant market data such as comparable public company trading multiples, recent M&A transaction comparables, and discount rates; and then applying one or more recognised methodologies such as earnings multiples, discounted cash flow analysis, or, where a recent transaction provides a reliable anchor, a price based on recent transaction approach. The methodology is clear and well served by established professional frameworks.

Moreover, portfolio monitoring and enterprise valuation methodologies are areas that receive considerable focus and attention from both GPs and LPs. In our experience, they are the better understood half of the portfolio valuation challenge. Demanding as this process already is, the hidden complexity and data challenge lies with the second half of the valuation.

Part 2: Deriving the fund’s equity value across its portfolio

The second component, translating enterprise value in a portfolio into the equity value attributable to the fund, is where the current systems, data, and processes fall short.

The reason why this is the case, particularly for private equity, is as follows:

- Private equity investments are almost never wholly owned by the fund. Management teams routinely hold a meaningful equity stake. Co-investors are increasingly prevalent, particularly at the large-cap end of the market, and club deals bring in multiple institutional investors alongside the lead fund.

- They are highly structured to ensure each investor’s returns are captured adequately. Each party typically holds instruments with distinct economic terms: preference shares, loan notes, PIK instruments, convertible securities, sweet equity, each with its own ranking in the capital structure, some coupon bearing, and with their own distribution terms.

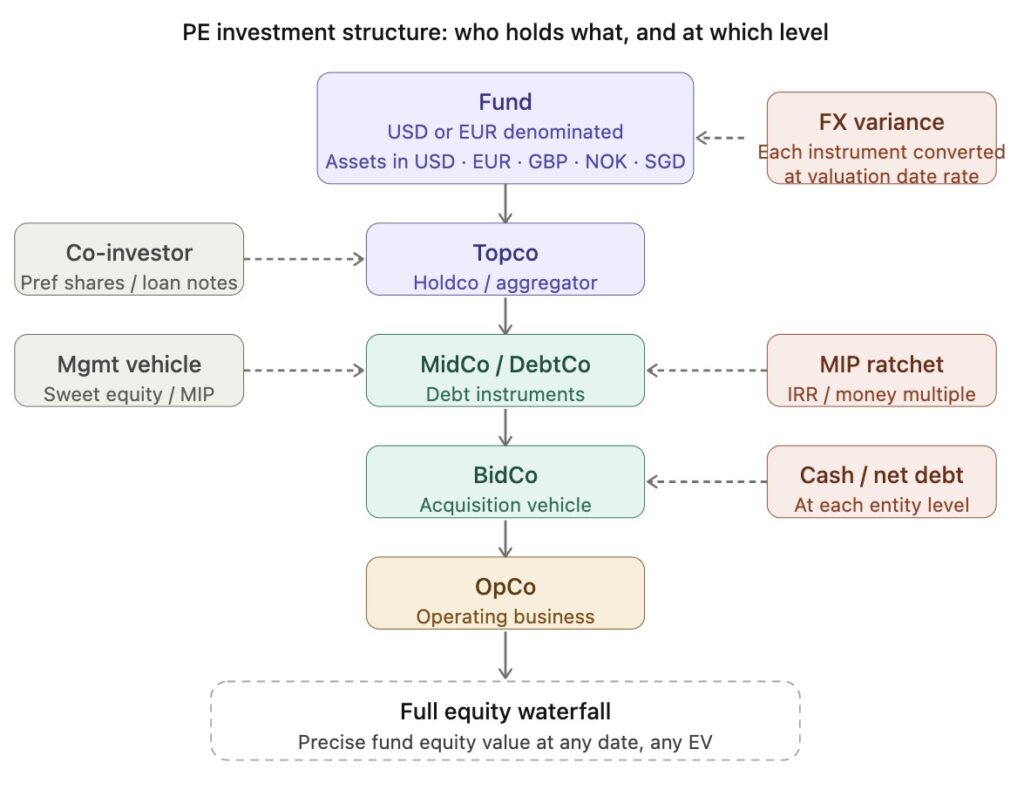

- They are often cross-border and require complex legal entity structures to achieve the desired tax and exit objectives. This complexity is rarely confined to a single legal entity. PE deal structures routinely span multiple entities in a chain: Aggregator vehicles and holding companies through to the operating business. Investors can often come in at different levels in the legal entity structure. It is also common for these structures to span multiple jurisdictions and currencies. Some intermediate entities may also hold cash balances or carry committed liabilities that affect the equity value ultimately available for distribution.

Given the above, there are broadly two approaches to valuing the fund’s equity across its portfolio:

The simplified approach applies the enterprise value against an ownership percentage derived from cap table data, using some form of economic or look-through ownership calculation. This is operationally manageable, particularly for a closed-end fund. It is rarely 100% accurate, because the economic reality is governed by multiple instruments, distribution rules, or performance-based ratchet mechanics rather than simple percentage ownership. But it suffices reporting needs, and the fund knows that the final economic outcome for investors crystallises on exit of a portfolio when the precise rules will be followed.

The full waterfall approach models the split of enterprise value through the entire capital structure, accounting for legal entity structures, instrument seniority, coupon accruals, participation rights, co-investor and management equity, to arrive at the precise equity value attributable to the fund. This is the correct approach. The reason many funds stop short of it comes down to operational reality. Based on conversations with GPs across our client base, having closely followed their systems and processes, the combined process of cap table management, equity valuations, audit support, and regulatory compliance already runs to multiple weeks’ work each quarter under current ways of working, with material additional burden during year-end audits and at exit. In the current excel based processes, generating full equity waterfall is highly manual and time consuming. To give some context to why a full portfolio-level equity waterfall is currently operationally unfeasible for a fund finance team: for a single asset at exit, external accountants or corporate finance advisors routinely spend days or weeks building and validating the full distribution waterfall model. Expecting a fund finance team to do this across an entire portfolio, every month, with full auditability, is a different proposition entirely.

But in an evergreen context, this may no longer be optional. The full process must run monthly rather than quarterly, and the fund must retain the ability to produce a defensible flash NAV at any point. Applied to an entire portfolio under current ways of working, the operational demand is significant, and that is before accounting for the higher accuracy bar that transactional NAV demands.

It is worth noting that NAV in a fund encompasses the fair value of portfolio investments, to take account of fund-level cash and liabilities, accrued expenses, fees, and carried interest obligations. It is also worth clarifying that “waterfall” in the fund context refers to the fund-level distribution waterfall that governs carried interest and distribution rules between the GP and LPs. The focus of this article is on the portfolio valuation and waterfall. The aggregate value of equity held by the fund across its portfolio is what ultimately underpins the fund level NAV.

Why getting this wrong is not an option for evergreen funds

For a closed-end fund, lack of precision in equity valuation is a meaningful error, but it is not a transactional one. It can nevertheless be a reputational issue with LPs and auditors, particularly if mistakes have to be corrected.

For an evergreen fund, there is no such correction mechanism. Investors are transacting periodically at the reported NAV. If that NAV is wrong, in either direction, investors are being harmed in real time.

The following are structural features of typical private equity deal structures that, if not captured correctly, produce incorrect NAV:

Management incentive structures. Management teams hold significant minority stakes in virtually every PE backed business, it is a defining feature of the asset class. Management Incentive Plans with sweet equity ratchets (common in Europe), or time and performance vested incentive units (common in US) are common. Whatever the structure or geography, the economic effect is the same across all markets: the value attributable to management, and therefore to the fund, is not a fixed percentage of enterprise value; it is a function of return performance. Despite this, funds rarely value management equity in detail during periodic reporting, largely because the data required to do so is difficult to track and maintain (e.g. it takes external advisor’s days / weeks to produce this during exits).

In practice, what we commonly see is management equity ratchets simply not being valued. The data required – detailed cap tables, changes over time, precise ownership terms and distribution rules – is often sitting in fragmented deal documents, and without the right systems, pulling it together for every portfolio company every quarter is cumbersome enough that it gets set aside.

In a closed-end fund, this can be tolerated as the exit resolves it. In an evergreen fund, not estimating the value of management incentive plans can overestimate the fund’s equity value across its portfolio.

Structured instruments: loans, preferred equity, reserves, coupons, and premiums. Beyond ordinary equity, PE investment structures routinely layer in a range of additional instruments: investor loans, preferred equity instruments, vendor loans, unallocated reserves, different classes of shares, participating instruments, and capital contributions, each introduced for tax, regulatory, or commercial structuring reasons. Each carries its own economic terms, including ranking, coupon rate, and participation rights, that determine how value is distributed in a waterfall. In an evergreen fund transacting at NAV, valuing these instruments correctly at every reporting date becomes important.

The most common errors we see in practice are mistakes in accruals and ranking order on coupon-bearing instruments through the structure, and unallocated or reserve shares being incorrect or excluded entirely, which directly overestimates the fund’s equity. We also frequently see capital events during the investment period: dividend recaps, add-on transactions, distributions, and cap table resets, not being accurately captured on an ongoing basis, which compounds the error over time.

Multi level entity structures. PE investments invariably sit within legal entity structures comprising multiple holding vehicles: Topco, HoldCo, BidCo, fund vehicles, co-investor vehicles, management vehicles, often spanning multiple jurisdictions, with different investors entering at different levels in the chain. Tracking each of these levels, all the way through to the fund, is essential to arriving at the correct equity value. In practice, intermediate entities may hold cash balances, or have committed expenses. In a closed-end fund, the operational burden of maintaining this granularity across the full portfolio every quarter is significant, and it is often not done in full. In an evergreen fund, this may no longer be an option.

FX variance. The fund’s reporting currency does not always match the currency in which a portfolio company’s capital structure is denominated. A USD or EUR denominated fund may have investments in the UK, Nordics, or Asia, where the underlying capital structures are denominated in GBP, NOK, or SGD. When valuing equity, each instrument and each invested amount needs to be converted into the reporting currency at the investment date, and resulting equity value converted to the reporting currency at the prevailing rate on the valuation date. This means that even where the underlying instrument values are unchanged, movements in exchange rates between valuation dates will affect the equity value reported in the fund’s currency. In a closed-end fund, FX movements are noted and disclosed but their impact on any single quarterly NAV is not transactional. In an evergreen fund, where investors are subscribing and redeeming at that NAV, FX variance in the equity valuation is a real and recurring source of pricing sensitivity that must be captured accurately at every reporting date.

None of these issues will necessarily have a material impact on any single portfolio company in any single quarter. But across a fund’s full portfolio, and compounded over time, the cumulative effect can be meaningful. In an evergreen structure, where NAV is the price at which investors transact rather than a periodic estimate, that cumulative drift may not be an acceptable margin of error.

Technology is not optional

The only way to meet the NAV demands of an evergreen PE fund – accuracy, frequency, audit ready, and defensible – is through a combination of technology and standardised processes. Evergreen funds are a risk to operate with fragmented data and manual processes. They don’t have the safety net of being able to correct quarterly estimates later or at portfolio exit.

This is the gap DealsPlus was built to address. Forward looking closed-end funds are already significant users of DealsPlus. But for evergreen funds, data accuracy and precision are non-negotiable. Our platform is purpose-built for PE investment structures across instruments, entities, and jurisdictions, with an automated portfolio-level waterfall engine that produces auditable equity valuations, however complex the structure.

We also know this first-hand, having implemented DealsPlus for private equity funds of all sizes and across geographies, that technology needs to be enabled with robust processes.

Our customer success team, drawn from PE tax and audit backgrounds, does three things that matter in practice. First, they take a fund’s fragmented ownership data, investment structures, and waterfall terms and build a coherent, validated structure within DealsPlus, identifying errors and gaps in existing data, which clients consistently tell us is one of the most valuable parts of the engagement. Second, they work with the fund’s stakeholders to implement robust workflows and automated sign-off processes that keep everything current between valuation cycles. Third, they ensure DealsPlus works smoothly across every use case the fund needs it for: equity valuation, annual audit, or exit modelling, including the ability to produce flash NAV on demand, something that simply is not achievable without a purpose built system.

On the evergreen side, we are working with some of the largest private equity managers globally, with growing evergreen strategy, who have told us directly that managing and reporting accurately for their evergreen funds would not be possible without a purpose-built system. We are actively working with them to demonstrate exactly how technology can bridge that gap.

Our goal is for every private equity firm to have the ability to accurately value portfolio equity anytime, however complex the structure.

To see DealsPlus in action, request a demo or visit dealsplus.io.