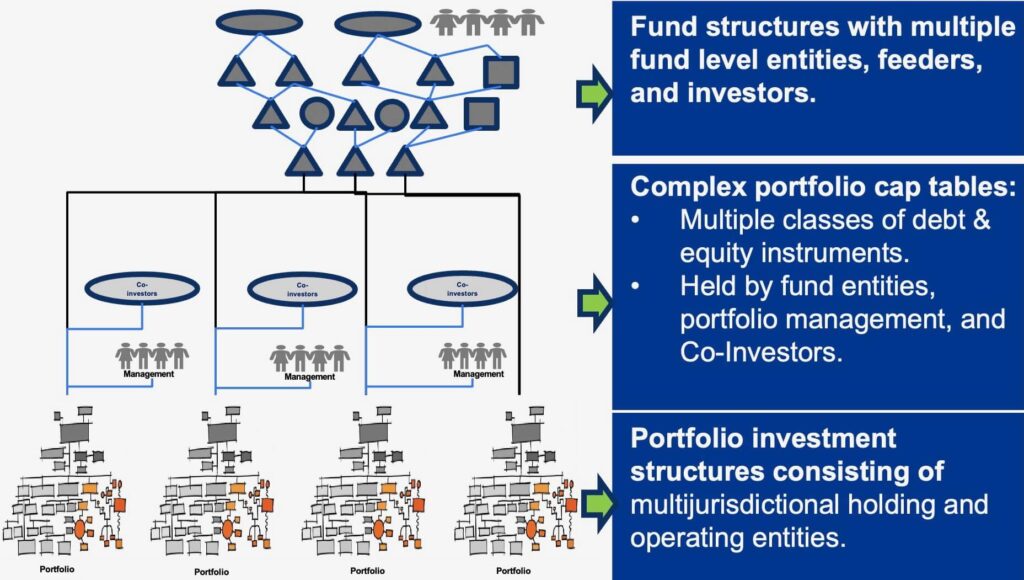

Private equity investment structures have multi-layered fund and portfolio structures which can make tracing the beneficial interest through the legal ownership chain challenging. Undertaking any task that requires tracing through the fund and portfolio investment structures to identify, allocate, and value the economic interest – e.g. fund valuation, UBO analysis, investor tax reporting – onerous and expensive.

There are three main reasons why tracing the economic ownership in private equity investment structures is challenging:

- Most private equity funds consist of multi-layered legal entity structures –separate fund vehicles for different investor types, feeder vehicles for specific investor(s), co-investment vehicles for the fund manager, and carried interest vehicles for manager’ performance fee.

- The fund itself invests in the portfolio companies either directly or via one or more holding companies. The portfolio level investment structures can get more complex when accommodating co-investors and portfolio management as shareholders as each group of investors may have their own intermediary holding / investment vehicles.

- Each private equity portfolio will have its own capital structure and equity plan consisting of multiple classes of equity and debt instruments (strip equity, sweet equity, and loans), with varying economic and control rights.

Private equity investment structure depicting multi-layered fund and portfolio structure

Given the above, it can be challenging to trace, allocate, and value the beneficial ownership interest. This can make the following tasks challenging:

- Fund reporting and valuation: Being able to track and value the equity interest across portfolio investments at the fund level.

- UBO and AML analysis: Portfolio companies need to analyse and prove UBO position with their lenders and/or external service providers. In addition, it is becoming increasingly likely that fund managers may need to maintain a register of all the legal entities under their control.

- Investor tax reporting and analysis: Being able to trace through multi-layered ownership structures, legal entity classifications, and financing arrangements will be relevant for fund level investor tax reporting and analysis – e.g. US K1s.

Connecting the dots between the legal chain and economic ownership

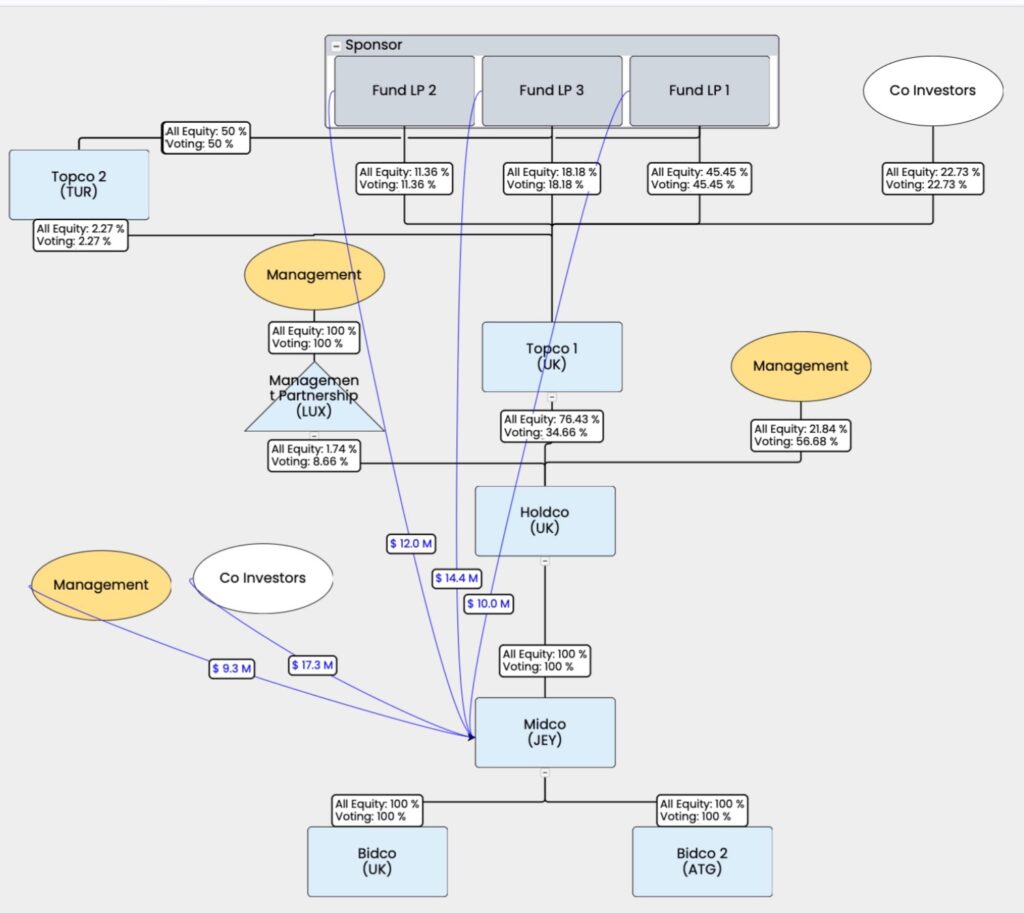

A software like DealsPlus, with its ability to digitise and administer fund and portfolio structures and cap tables, can help navigate these challenging tasks with ease. Here’s an example of a private equity portfolio structure managed in DealsPlus:

In this structure:

- The private equity fund – via multiple fund vehicles – is invested in the Portfolio Company via a series of holding companies.

- The portfolio company also has direct and indirect investment from a Co-investor(s) and the portfolio management team.

- The Portfolio Company’s capital structure (equity plan) consists of strip equity, sweet equity, and loan instruments – each with varying economic and control rights. The Fund entities and Co-investors hold most of the strip equity and loans, with management mostly invested in the sweet equity.

The effective ownership for a structure like this would trace through this legal chain and allocate the ownership in the Portfolio Company’s capital structure to each beneficial owners – i.e., each of the fund entities, co-investor, and management holders.

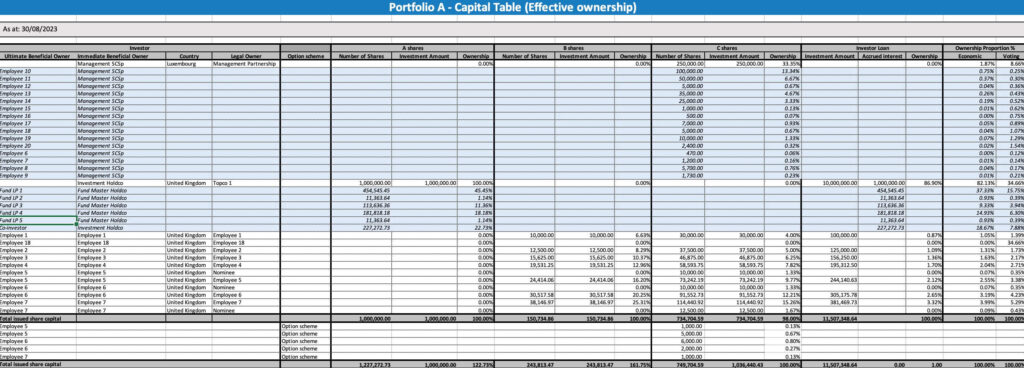

DealsPlus helps allocate the effective ownership in the portfolio equity plan to beneficial owner.

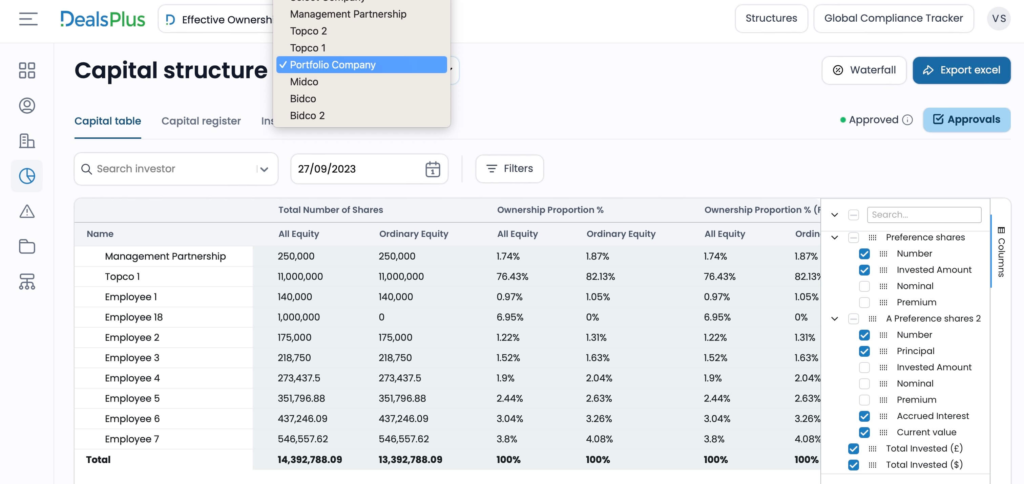

By connecting the dots across fund and portfolio structures, and helping digitise and administer portfolio equity plans, DealsPlus helps simplify fund valuation, UBO analysis, and investor reporting.